| Arete Quarterly Q113 |

Welcome

There is a saying that generals always fight the last war, which holds especially true if they’ve won it. Back in the middle of the twentieth century, America’s industrial prowess was an incredibly important factor in the victory by allied forces in World War II. There was no doubt that the massive quantities of ships, aircraft and armaments that American industry produced were critical to prevailling in a war spanning multiple fronts across three continents.

As with many things, however, the nature of armed conflict has changed dramatically over the past several decades. This change was foreshadowed in Vietnam and was clearly evident in the 9/11 attacks on the World Trade Center towers. It has also been demonstrated in a wide variety of other incidents across the globe since. The spectacle of collossal clashes has been supplanted by surgical strikes.

As the nature of attacks has evolved, so too have the responses. This was neatly demonstrated in the recent movie, Zero Dark Thirty. Notably, the effective effort of tracking down the intelligent and highly elusive target of Osama Bin Laden was not due to masses of people and machinery. Instead, what worked was basically a single, dedicated CIA agent and a Navy Seal team.

These lessons from warfare have application to the investment management business. Many investment firms that were created in more fruitful economic times and in more tranquil capital markets built massive distribution networks and research departments. In the context of high and persistent returns and new money inflows, the high costs of building and maintaining such mammoth structures were outweighed by the benefits of simply providing exposure to such broad opportunities.

In today’s world of low real returns and sketchy economic prospects, however, many incumbent investment firms seem poorly suited to win today’s investment battles. Spending lots of money to amass piles of information does a lot less towards making investors better off than does thoughtfully and efficiently piecing it together and adroitly acting on opportunity. Nonetheless, many investors continue to be impressed by the grand profiles large firms present in fighting the last war.

Arete is different from many of its competitors in that it is not big nor does it aspire to be. It is purpose-built to find attractive stock picks and is dedicated to doing this well. It is also driven by the mission of ensuring that clients benefit from its efforts and end up better off. In these respects, Arete is not fighting past investment wars like so many others, but rather is fighting current wars and constantly adapting for future ones.

There is a saying that generals always fight the last war, which holds especially true if they’ve won it. Back in the middle of the twentieth century, America’s industrial prowess was an incredibly important factor in the victory by allied forces in World War II. There was no doubt that the massive quantities of ships, aircraft and armaments that American industry produced were critical to prevailling in a war spanning multiple fronts across three continents.

As with many things, however, the nature of armed conflict has changed dramatically over the past several decades. This change was foreshadowed in Vietnam and was clearly evident in the 9/11 attacks on the World Trade Center towers. It has also been demonstrated in a wide variety of other incidents across the globe since. The spectacle of collossal clashes has been supplanted by surgical strikes.

As the nature of attacks has evolved, so too have the responses. This was neatly demonstrated in the recent movie, Zero Dark Thirty. Notably, the effective effort of tracking down the intelligent and highly elusive target of Osama Bin Laden was not due to masses of people and machinery. Instead, what worked was basically a single, dedicated CIA agent and a Navy Seal team.

These lessons from warfare have application to the investment management business. Many investment firms that were created in more fruitful economic times and in more tranquil capital markets built massive distribution networks and research departments. In the context of high and persistent returns and new money inflows, the high costs of building and maintaining such mammoth structures were outweighed by the benefits of simply providing exposure to such broad opportunities.

In today’s world of low real returns and sketchy economic prospects, however, many incumbent investment firms seem poorly suited to win today’s investment battles. Spending lots of money to amass piles of information does a lot less towards making investors better off than does thoughtfully and efficiently piecing it together and adroitly acting on opportunity. Nonetheless, many investors continue to be impressed by the grand profiles large firms present in fighting the last war.

Arete is different from many of its competitors in that it is not big nor does it aspire to be. It is purpose-built to find attractive stock picks and is dedicated to doing this well. It is also driven by the mission of ensuring that clients benefit from its efforts and end up better off. In these respects, Arete is not fighting past investment wars like so many others, but rather is fighting current wars and constantly adapting for future ones.

Business Update

There are many different stories about why people start their own investment firms. Some always wanted to be entrepreneurs. Some wanted to make bucket-loads of money. Some just wanted a nice, comfortable lifestyle in which they could call the shots.

For me, it was always about being a great investor. This wasn’t just a nice idea; it was an economic imperative. Starting with a pile of student loans instead of a wad of family money, I knew the best thing I could do to materially improve my lot in life was to save and invest well. As a result, investing takes on a special place in my psyche. I see it not just as an academic exercise but as a means of realizing a better life.

Interestingly, as my investment knowledge and expertise increased over the years, my belief in the value of most of the investment products I encountered decreased. I certainly didn’t find many that I felt comfortable putting much of my own money in.

It wasn’t that there weren’t talented people out there. There were plenty. I think it is more accurate to say that what I found (and still find) were services that were compelling in one dimension, but not in other important ones. For example, hedge funds were very performance-oriented, but tended to be expensive, illiquid and inaccessible. Mutual funds were liquid and accessible, but had low active share which significantly diminished performance opportunities. Institutional separate accounts were more secure, but only available to the largest institutions.

Since I didn’t find any options that met my high standards, I started investing in stocks myself. Mainly I wanted to further benefit from what I believed to be the fairly strong set of investment skills I was developing, other than just by receiving compensation for my job. I also thought it would be a good lesson to learn what it felt like to have my own money on the line.

Although I started in early 2000 at perhaps one of the worst times to enter equity markets, my valuation work successfully directed me away from technology stocks and towards energy stocks (I didn’t have the money to invest earlier because I was paying off student loans). As a result, I managed to substantially increase my personal holdings during a time in which the S&P 500 was flat to down. This experience was extremely beneficial to me because it ultimately gave me both the funds and the confidence to found Arete.

As I consider business development efforts today, I am sharing with other investors the course of action I am taking myself. In short, I continue turning over a lot of rocks to find great stock ideas, but the fact remains that there aren’t a lot given the huge run-up in prices. As a consequence, I still have quite a bit of cash ready to deploy as great opportunities emerge.

One of the negative consequences of low real rates of return is that investing in financial assets under these conditions does not make you significantly better off. In many cases, the risks taken are outweighed by the meager benefits. It may end up preserving some wealth that otherwise would be lost to inflation or other means, but it does not leave you in a better place.

While it is fair to say I am pretty intensely dissatisfied with this situation, it is also fair to say I don’t intend to accept it passively. Given limited opportunities with financial assets right now, it makes sense to consider other forms of wealth, of which knowledge can be considered one in a very broad sense. Indeed, at these low interest rates we have a unique situation in which there is essentially no opportunity cost for acquiring knowledge.

As a result, I have been making extra efforts to step up my learning experiences. Much of this I have been accumulating in the AreteResearch site, but I have also been preparing presentations on topics I believe can be especially helpful for investors. Some of this can help create context for the investment environment, some of it can help combat misinformation, and some of it can present useful courses of action for various investors.

Because I believe there are so many potential uses of the insights gleaned from my efforts, and because this is a great time to pursue them, I am renewing efforts to talk to investors, to share this knowledge, and to build new relationships. I am still leery as to the intermediate term opportunity for stocks given current valuations, and don’t plan on chasing the market. But this is a very good time to learn and prepare and I recommend other investors do the same. At very least, it is also a great opportunity to learn more about what Arete is and how it works.

If you, someone you know, or some group with which you are familiar, may be interested in hearing more about Arete or any of several different general subjects about investing, please let me know and we can work something out.

Thanks and take care!

David Robertson, CFA

CEO, Portfolio Manager

There are many different stories about why people start their own investment firms. Some always wanted to be entrepreneurs. Some wanted to make bucket-loads of money. Some just wanted a nice, comfortable lifestyle in which they could call the shots.

For me, it was always about being a great investor. This wasn’t just a nice idea; it was an economic imperative. Starting with a pile of student loans instead of a wad of family money, I knew the best thing I could do to materially improve my lot in life was to save and invest well. As a result, investing takes on a special place in my psyche. I see it not just as an academic exercise but as a means of realizing a better life.

Interestingly, as my investment knowledge and expertise increased over the years, my belief in the value of most of the investment products I encountered decreased. I certainly didn’t find many that I felt comfortable putting much of my own money in.

It wasn’t that there weren’t talented people out there. There were plenty. I think it is more accurate to say that what I found (and still find) were services that were compelling in one dimension, but not in other important ones. For example, hedge funds were very performance-oriented, but tended to be expensive, illiquid and inaccessible. Mutual funds were liquid and accessible, but had low active share which significantly diminished performance opportunities. Institutional separate accounts were more secure, but only available to the largest institutions.

Since I didn’t find any options that met my high standards, I started investing in stocks myself. Mainly I wanted to further benefit from what I believed to be the fairly strong set of investment skills I was developing, other than just by receiving compensation for my job. I also thought it would be a good lesson to learn what it felt like to have my own money on the line.

Although I started in early 2000 at perhaps one of the worst times to enter equity markets, my valuation work successfully directed me away from technology stocks and towards energy stocks (I didn’t have the money to invest earlier because I was paying off student loans). As a result, I managed to substantially increase my personal holdings during a time in which the S&P 500 was flat to down. This experience was extremely beneficial to me because it ultimately gave me both the funds and the confidence to found Arete.

As I consider business development efforts today, I am sharing with other investors the course of action I am taking myself. In short, I continue turning over a lot of rocks to find great stock ideas, but the fact remains that there aren’t a lot given the huge run-up in prices. As a consequence, I still have quite a bit of cash ready to deploy as great opportunities emerge.

One of the negative consequences of low real rates of return is that investing in financial assets under these conditions does not make you significantly better off. In many cases, the risks taken are outweighed by the meager benefits. It may end up preserving some wealth that otherwise would be lost to inflation or other means, but it does not leave you in a better place.

While it is fair to say I am pretty intensely dissatisfied with this situation, it is also fair to say I don’t intend to accept it passively. Given limited opportunities with financial assets right now, it makes sense to consider other forms of wealth, of which knowledge can be considered one in a very broad sense. Indeed, at these low interest rates we have a unique situation in which there is essentially no opportunity cost for acquiring knowledge.

As a result, I have been making extra efforts to step up my learning experiences. Much of this I have been accumulating in the AreteResearch site, but I have also been preparing presentations on topics I believe can be especially helpful for investors. Some of this can help create context for the investment environment, some of it can help combat misinformation, and some of it can present useful courses of action for various investors.

Because I believe there are so many potential uses of the insights gleaned from my efforts, and because this is a great time to pursue them, I am renewing efforts to talk to investors, to share this knowledge, and to build new relationships. I am still leery as to the intermediate term opportunity for stocks given current valuations, and don’t plan on chasing the market. But this is a very good time to learn and prepare and I recommend other investors do the same. At very least, it is also a great opportunity to learn more about what Arete is and how it works.

If you, someone you know, or some group with which you are familiar, may be interested in hearing more about Arete or any of several different general subjects about investing, please let me know and we can work something out.

Thanks and take care!

David Robertson, CFA

CEO, Portfolio Manager

Market Overview

Hope springs eternal and especially so as springtime approaches it seems. Notably, the return of the Russell Midcap Index® for each of the last four first quarters (Q113: 12.96%, Q112: 12.94%, Q111: 7.63%, Q110: 8.67%) was significantly better than would normally be expected for an entire year.

Indeed, for each of the three complete years 2010 – 2012, the first quarter’s return comprised a significantly disproportionate share of the year’s return. The first quarter in 2012, for example, comprised nearly three-quarters of the annual return and in 2011 the return was negative for the year.

The Fed, through its easy money policy, is clearly trying to arm-twist any remaining risk-averse (we would say “prudent”) investors into capitulation. This has created a great deal of temptation worth addressing.

While we are contrarian by nature, we are far from the only ones reluctant to completely give in to that pressure. The evidence of increasing disparities between weak economic fundamentals and high market valuations has been far too great to ignore. A useful characterization of this paradox was coined by noted economist, Gary Shilling, as the “Grand Disconnect.”

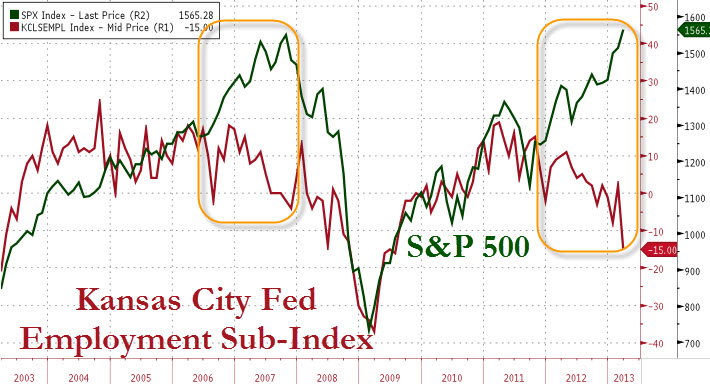

One of the research pieces we came across recently that illustrates the “Grand Disconnect” especially well was posted on the ZeroHedge.com website and is displayed below (though there are a huge number of graphs portraying similar stories). It shows the relationship between employment (which is a good proxy for economic health) and the S&P 500 index over the last ten years. The graph depicts clearly that what is happening in the real economy is completely different from what is happening in the market (Source: ZeroHedge.com).

Of course this has happened in the past as also shown in the graph. In late 2006, the S&P 500 continued its run upward while employment flattened and eventually dropped significantly. Eventually the two patterns converged when the S&P 500 fell precipitously to “reconnect” with employment trends.

Recent comments by a couple of excellent investors on CNBC and reported by ZeroHedge.com illustrate what this means for investors. Sam Zell said, “The current stock market feels like the housing market of 2006. Everybody can't afford to miss it." He continued, “Every single day it [the market] goes up. What were the headlines in 2006 - housing prices going up every day. What are you talking about every day now - new high in stocks every day!” David Rosenberg of Gluskin Sheff also provided his perspective: “You could have fought the Fed in 2000 and 2009 and done quite well... [thanks to the Fed] the market will tend to drift up - until something breaks.”

This encapsulates well the challenges for investors. Your two main choices are feeling like you “can’t afford to miss it” and jumping on the bandwagon, or waiting “until something breaks,” and suffering negative real rates of return on cash during the interim. Given that our normal policy is to be fully invested, let’s examine the logic required to justify such a position now.

In order to go all-in with stocks, you would first need to have confidence that the current ride is going to last long enough to make it worth your while. Second, you would want to make sure you could get out before the market reversed. Finally, you would need to have a good idea of the things could go wrong and the magnitude of losses if they did.

While it probably is fair to assume that the Fed will continue its program of quantitative easing for some time, it is far less clear whether this will lead to further gains in the market. For one, earnings do matter and have been under pressure despite record high margins. Also, it may become evident to the market, and perhaps even to the Fed itself, that its policies are either ineffective or counterproductive in helping employment growth. In addition, there remain a great many exogenous risks across the world that could rapidly quell risk-taking at any time irrespective of central bank policy.

Underlying all of these conditions is a credit market significantly comprised of shadow banking activities. These forms of credit differ materially from credit created through the fractional reserve banking system in that there is no reserve. They work as long as asset prices keep going up, but they collapse when asset prices fall (i.e., when “something breaks”). Noted economist, Hyman Minsky, called such systems, “Ponzi finance” to capture their salient features.

As a reminder, the financial crisis of 2008.2009 was precipitated by problems in the shadow banking sector. This is why problems that started with the relatively small subprime housing sector became much, much bigger. Unfortunately the structure of the credit market has not changed a great deal and there are many signs of resurgence in shadow banking.

What this means for investors is that the system is still quite fragile. When things do go down, they can go down a lot, and quickly. Forced sellers jam the exit doors because they must get out at any price. This is exacerbated by the vast interconnectedness global financial institutions which enables problems to cascade quickly from almost anywhere in the world.

The main point of outlining this is to highlight the logical flaws of undue exuberance for stocks right now. It doesn’t change the fact that bonds look even riskier over long investment horizons.

What does follow fairly naturally from this discussion are a couple of constructive courses of action for investors to consider. First and foremost is to be wary of playing the market as a whole; this has become an especially dangerous game. Conversely, it is a great time to be looking for stocks that don’t necessarily move with the market, but can perform on their own merits. There are always stocks that work and the mid cap universe is especially flush with interesting and dynamic companies. Don’t let some of the headwinds of the market environment overshadow the real opportunities to produce attractive returns.

Another useful pursuit is to manage the fragility in financial markets. Because a lot of different financial assets can be hurt at these prices, it makes sense to avoid significant concentrations. If there is one thing to avoid, it is any notion that anyone has an incredibly clear idea of the ultimate outcome of these conditions.

Finally, it is a good time to seriously consider ways to better manage against inflation if you haven’t already. Inflation is not a big problem today, but the chances are good that it will be over a long investment horizon. It’s hard to conceive today, but the dollar lost half of its value through inflation over four years from 1978 – 1981. Largely because it’s hard to conceive today, though, the costs of protection are fairly attractive.

Hope springs eternal and especially so as springtime approaches it seems. Notably, the return of the Russell Midcap Index® for each of the last four first quarters (Q113: 12.96%, Q112: 12.94%, Q111: 7.63%, Q110: 8.67%) was significantly better than would normally be expected for an entire year.

Indeed, for each of the three complete years 2010 – 2012, the first quarter’s return comprised a significantly disproportionate share of the year’s return. The first quarter in 2012, for example, comprised nearly three-quarters of the annual return and in 2011 the return was negative for the year.

The Fed, through its easy money policy, is clearly trying to arm-twist any remaining risk-averse (we would say “prudent”) investors into capitulation. This has created a great deal of temptation worth addressing.

While we are contrarian by nature, we are far from the only ones reluctant to completely give in to that pressure. The evidence of increasing disparities between weak economic fundamentals and high market valuations has been far too great to ignore. A useful characterization of this paradox was coined by noted economist, Gary Shilling, as the “Grand Disconnect.”

One of the research pieces we came across recently that illustrates the “Grand Disconnect” especially well was posted on the ZeroHedge.com website and is displayed below (though there are a huge number of graphs portraying similar stories). It shows the relationship between employment (which is a good proxy for economic health) and the S&P 500 index over the last ten years. The graph depicts clearly that what is happening in the real economy is completely different from what is happening in the market (Source: ZeroHedge.com).

Of course this has happened in the past as also shown in the graph. In late 2006, the S&P 500 continued its run upward while employment flattened and eventually dropped significantly. Eventually the two patterns converged when the S&P 500 fell precipitously to “reconnect” with employment trends.

Recent comments by a couple of excellent investors on CNBC and reported by ZeroHedge.com illustrate what this means for investors. Sam Zell said, “The current stock market feels like the housing market of 2006. Everybody can't afford to miss it." He continued, “Every single day it [the market] goes up. What were the headlines in 2006 - housing prices going up every day. What are you talking about every day now - new high in stocks every day!” David Rosenberg of Gluskin Sheff also provided his perspective: “You could have fought the Fed in 2000 and 2009 and done quite well... [thanks to the Fed] the market will tend to drift up - until something breaks.”

This encapsulates well the challenges for investors. Your two main choices are feeling like you “can’t afford to miss it” and jumping on the bandwagon, or waiting “until something breaks,” and suffering negative real rates of return on cash during the interim. Given that our normal policy is to be fully invested, let’s examine the logic required to justify such a position now.

In order to go all-in with stocks, you would first need to have confidence that the current ride is going to last long enough to make it worth your while. Second, you would want to make sure you could get out before the market reversed. Finally, you would need to have a good idea of the things could go wrong and the magnitude of losses if they did.

While it probably is fair to assume that the Fed will continue its program of quantitative easing for some time, it is far less clear whether this will lead to further gains in the market. For one, earnings do matter and have been under pressure despite record high margins. Also, it may become evident to the market, and perhaps even to the Fed itself, that its policies are either ineffective or counterproductive in helping employment growth. In addition, there remain a great many exogenous risks across the world that could rapidly quell risk-taking at any time irrespective of central bank policy.

Underlying all of these conditions is a credit market significantly comprised of shadow banking activities. These forms of credit differ materially from credit created through the fractional reserve banking system in that there is no reserve. They work as long as asset prices keep going up, but they collapse when asset prices fall (i.e., when “something breaks”). Noted economist, Hyman Minsky, called such systems, “Ponzi finance” to capture their salient features.

As a reminder, the financial crisis of 2008.2009 was precipitated by problems in the shadow banking sector. This is why problems that started with the relatively small subprime housing sector became much, much bigger. Unfortunately the structure of the credit market has not changed a great deal and there are many signs of resurgence in shadow banking.

What this means for investors is that the system is still quite fragile. When things do go down, they can go down a lot, and quickly. Forced sellers jam the exit doors because they must get out at any price. This is exacerbated by the vast interconnectedness global financial institutions which enables problems to cascade quickly from almost anywhere in the world.

The main point of outlining this is to highlight the logical flaws of undue exuberance for stocks right now. It doesn’t change the fact that bonds look even riskier over long investment horizons.

What does follow fairly naturally from this discussion are a couple of constructive courses of action for investors to consider. First and foremost is to be wary of playing the market as a whole; this has become an especially dangerous game. Conversely, it is a great time to be looking for stocks that don’t necessarily move with the market, but can perform on their own merits. There are always stocks that work and the mid cap universe is especially flush with interesting and dynamic companies. Don’t let some of the headwinds of the market environment overshadow the real opportunities to produce attractive returns.

Another useful pursuit is to manage the fragility in financial markets. Because a lot of different financial assets can be hurt at these prices, it makes sense to avoid significant concentrations. If there is one thing to avoid, it is any notion that anyone has an incredibly clear idea of the ultimate outcome of these conditions.

Finally, it is a good time to seriously consider ways to better manage against inflation if you haven’t already. Inflation is not a big problem today, but the chances are good that it will be over a long investment horizon. It’s hard to conceive today, but the dollar lost half of its value through inflation over four years from 1978 – 1981. Largely because it’s hard to conceive today, though, the costs of protection are fairly attractive.

RSS Feed

RSS Feed